EU BLOCKS RUSSIAN OIL

On May 30th, the Heads of State of the European Union decided on the sixth packageof sanctions imposed on Russia, including the blockade of Russian oil on Europe, affecting the supply of 4.1 million barrels per day between oil and petroleum products.

The decision was preceded by strong political pressure from both the U.S. and E.U. member countries, who, through the president of the European Commission (E.C.) Úrsula Von der Leyer, European Council President Charles Michell and EC Chancellor Josep Borrell have insisted, since the beginning of the conflict, on including in the E.U. sanctions packages on Russia the blockade of both oil and gas supplies.

Other European countries have successively contained these pressures because of the impact they would have on their economies until the E.U. finally agreed to block both oil and petroleum products (especially diesel and gasoline) from Russia.

The measure will enter fully into force from June and will be completed over the next six months and affects directly Russian oil and products supply to Europe by sea (2.8 million barrels per day, 67 % of their demand), temporarily excluding oil volumes transported via pipelines (1.3 million barrels per day). However, E.C. President Úrsula Von der Leyer said in her announcement of the blockade that the E.U. expects the E.U. to reach 90 % of current supplies by the end of the year.

The exclusion from supply via pipelines responded to a demand from the Prime Minister of Hungary, Viktor Orbán, who threatened to veto the decision if he could not receive Russian oil through the Druzhba pipeline, as his country has no access to the sea.

The decision to block the supply of Russian oil to Europe — in addition to politicising the issue of energy — introduces to the oil market a strong factor of uncertainty and risk in supply that has been immediately reflected in the oil prices that were quoted upwards on May 30th, Brent opened at $123.82 a barrel, while WTI did so at $118.85 a barrel, an increase of 2.15 % and 3.88 % respectively.

The blockade of Russian oil in Europe adds to the massive economic sanctions that have the declared purpose of the E.U. authorities to break the Russian economy by affecting its oil and gas exports, amounting to revenues of approximately 270 billion dollars per year for the Russian Federation.

The sixth E.U. sanctions package includes exclusions of more Russian banks from the Swift payment system, including Sberbank, and restrictions on chartering and insurance of ships carrying oil and Russian products.

It is important to note that the volumes of oil and products of Russia and Iran, subject to sanctions or blockades for political reasons, currently reach 6 million barrels per day, representing 6.1 % of demand in the second quarter of the year, which — in the absence of additional or surplus oil supply capacities — is a permanent factor of pressure on the price that has kept Brent and WTI scorers above 110 dollars a barrel.

It seems that we are in the presence of a kind of “deglobalisation” of the oil market, a phenomenon that — contrary to the deIt seems that we are in the presence of a kind of “deglobalisation” of the oil market, a phenomenon that — contrary to the development of the economy in recent decades — will affect the performance of the world economy by making energy costs more expensive.

OPEC+

At its 29th Ministerial Meeting on June 2nd, OPEC+, although in its declaration ratified the flexibilisation mechanism, decided to advance the planned adjustment for September, which will be distributed in the volume of the adjustments corresponding to July and August, which will increase 216 thousand barrels per day, leaving, each month, 648 thousand barrels per day.

With this decision, OPEC+ makes an additional (modest) increase in its monthly production, anticipating a fall in Russia’s production and yielding to political pressures by the U.S. and the E.U. to make use of its surplus production capacity amid a market where the barrel of oil — subject to pressure from geopolitical factors — remains at prices above $110 a barrel.

It seems that the OPEC+ decision, which seeks to alleviate political pressure on the countries of the Persian Gulf, will not have a significant effect on the price of oil, increasing supply because — except for Saudi Arabia and the UAE — the countries of the group have presented problems in increasing their production and has remained below the agreed quotas in the last nine months.

However, political pressure on OPEC continues, particularly among the Gulf monarchies and Saudi Arabia — the group’s de facto leader. U.S. President Joe Biden announced a visit to Saudi Arabia by the end of the month to meet Prince Mohammed Bin Salman, about whom Biden himself and the Democrats had made severe remarks about the murder of journalist Jamal Khashoggi.

The White House now seeks to ensure that the Saudi kingdom maximises its oil production and breaks with the close coordination and alliance with Russia within OPEC+.

So far, OPEC has maintained its position of not getting involved in political affairs and not politicising oil, which has allowed the organisation to survive the bloody conflicts and permanent pressures that have affected the Middle East in its history. It will be necessary to see whether the Gulf countries — in particular Saudi Arabia — will be able to uphold this principle amid the intense pressure from the U.S. and Europe against Russia.

Impact on market fundamentals

The E.U.’s blockade on Russian oil is a strong geopolitical element that adds to other factors that put pressure on the market, in addition to war and sanctions, which directly affect oil supply; demand has been affected by the decline in the global economy impacted by inflation and the resurgence of COVID in China.

These elements combine and threaten to break the balance of the oil market achieved throughout 2021-2020 thanks to the intervention of OPEC+. Geopolitical factors continue to erode the balance between supply and demand in the oil market.

On May 12th, both OPEC and the International Energy Agency (IEA) published data indicating that, due to the impact on Russia’s oil exports, as of April, there was a drop of 900 thousand barrels per day in its production, 9 % of its production, which had remained unchanged, in the 10 million barrels day of oil, until March.

Although Russian authorities have reported that production levels have recovered during May, it is the first time the effects of sanctions on the oil giant are reflected concretely.

However, in the latest OPEC Market Monitoring Report of May, the Organisation predicts, in its oil production estimates for 2022, that Russia’s production will fall by 360 million barrels per day, and I averaged 9.6 million barrels per day for the year, are estimated data that the Organisation considers to be subject to “great uncertainty.”

OPEC+, affected by the fall in Russia, reports a reduction of 800 thousand barrels per day in its oil supply in April due to the fall in production in Russia, Libya and Kazakhstan.

The U.S. and the countries grouped in the IEA have attempted to artificially increase the supply of crude oil with massive releases of oil from Strategic Reserves (SPRs) to reduce the impact of the geopolitical situation on the price to protect their economies from the inflationary impact of energy. The Biden administration has announced the release of 273 million barrels of oil to the market, while other consumer countries grouped in the IEA have announced the release of 60 million barrels of oil from their reserves.

However, since the beginning of the war, the price has remained in a high band ranging from $100-115 a barrel, with peaks of $138 a barrel. With the E.U.’s blockade of Russian oil, this band is likely to rise to stay between $110-120 a barrel. It is geopolitics that determines the price and a factor that is affecting, as a result, the world economy and demand for oil.

The world economy has given clear signs of decline, losing ground, after the post-COVID recovery of 2021 and which at the beginning of the year projected economic growth of 4.4 points.

The International Monetary Fund, in its latest reportof April 19th, estimated a contraction of 0.8 points in the world economy by 2022, placing it at 3.6 points; meanwhile, OPEC, in its May report, projects a growth of 3.5 % in the world economy, which shows a contraction of 0.7 points compared to its forecast for the beginning of the year.

In turn, the U.N. Department of Economic and Social Affairs, in its Update Reportof May 18th, estimated that the annual growth of the world economy would contract 0.9 points, from its estimates at the beginning of the year, to 3.1 %. In Europe, the same report estimates a drop of 1.2 points to 2.7 %, while a decline of 0.9 points is estimated to stand at 2.6 % for the U.S. economy. For the Chinese economy, growth is projected at 4.5 %, reflecting a decrease of 0.7 points from the year’s start estimates.

The fall of the economy in industrialised and energy-intensive countries is a direct effect of the war in Ukraine, the massive economic sanctions imposed on Russia, as well as the effects of COVID: the disruption of the supply chain, rising inflation in the U.S., the U.K. and Europe, and the unexpected resurgence of COVID in China, which led to drastic and massive confinement measures; all of which has finally affected the world’s demand for oil.

In its May Report, OPEC estimated the demand for the second quarter of the year at 98.4 million barrels per day, a drop of 670 thousand barrels per day from the 99.3 million barrels per day of demand estimated in April for the same period.

The slowdown of the economy, sanctions and the geopolitical situation in Europe has led to a fall in global oil demand, which has recovered considerably since the last quarter of 2020 (94.3 million barrels per day) and recovered by the fourth quarter of 2021 (100.3 million barrels per day), higher than 2019 (99.98 million barrels per day).

Estimates from OPEC, the International Energy Agency (IEA) and the U.S. Energy Information Administration in their May reports point to a demand reduction between 480 thousand barrels per day and 1.2 million barrels per day for 2022, placing it between 101.9 and 102.6 million barrels at the end of the year; a reduction of 600 thousand barrels per day from pre-war estimates.

Despite all the tensions in the economy, these demand values are very high, indicating that the price will continue to rise throughout this year due to restrictions on oil supply.

THE GAS WAR

Gas has become a crucial factor in the war between Russia-Ukraine and Europe’s geopolitical decisions. Europe’s high dependence on gas supplies from Russia has given the parties to the conflict, but above all, Russia, a negotiating instrument and a capacity to contain an escalation of sanctions or the same military conflict, which has influenced the course of the war.

Although the gas to Europe is supplied from Russia, the transit through the large pipelines that cross the continent, with Ukraine as territory of passage, given to the parties elements of negotiation and political pressure while providing them with resources, both for sale and the right of passage for gas, despite the bloody conflict and rhetoric of the parties.

The gas market in Europe is under extreme geopolitical tension after the war in Ukraine. As Europe is highly dependent on gas imports, equivalent to 95 % of its consumption, and Russia supplies 38 %, the political decisions and sanctions imposed on Moscow by the European Union have excluded any measure affecting the Russian gas supply.

Gas prices on the European market have been pushed upwards since the second half of 2021, resulting from the need for energy for the Post-COVID economic recovery, the lack of transport infrastructure development, bottlenecks and transmission restrictions and a low level of gas inventories in Europe. On the other hand, international LNG prices have been pressured upward by the gas requirements of Asian economies, which are also committed to their economic recovery.

From June 2021 to March 7th 2022, the gas price in Europe increased by more than 700 %, with a strong impact on the inflationary phenomenon in the euro area.

So far, there has been no suspension of gas supplies to Europe from Russia, while European companies have adapted to the payment of the invoice in rubles as demanded since Moscow. The Kremlin announced the suspension of the gas supply to Finland and Poland, both for its refusal to pay in rubles and the Finnish request to join NATO.

For the European economy, it is vital to continue to receive Russian gas in the face of the impossibility of replacing it in the short term. However, seems to be a political consensus among the member countries to stop depending on the infrastructure network that connects European countries with the world’s largest gas producer, an infrastructure that has been developing for more than 50 years — since the time of the former Soviet Union and Europe’s “distension” policy — and which mainly crosses the territory of Ukraine.

Two of the most important European countries with greater economic weight, Germany and Italy, emerged as the most dependent on Russian gas supplies. With a high degree of industrialisation, both countries have counted on gas as an abundant energy source for their electrical, industrial, and manufacturing sectors.

The E.U. Executive Committee has put forward successive plans to “independence” Europe from Russian gas supply, plans based on the premise of disconnecting completely from supplies from Russia, which — at the moment — does not seem feasible.

There are no sources or volumes of gas capable of replacing Russian-sourced gas, nor the transport infrastructure — whether by pipeline or LNG — sufficient to do so. This, despite the diplomatic and business activity that countries like Italy have developed in other gas-producing countries in Africa and the Middle East to ensure the supply of volumes to replace Russian gas.

Qatar’s oil minister, the world’s second-largest exporter of LNG, said on March 25th that «Russia provides, I believe, between 30 and 40 per cent of the supply to Europe. No country can replace that type of volume. There is no capacity to do so with LNG”. He added a key element of the LNG market: «Most LNG is linked to long-term contracts and very clear destinations. So replenishing that volume so fast is almost impossible.«.

U.S. LNG supply to Europe.

As of 2021, the US has become the world’s first LNG exporter from its surplus production of Shale Gas, displacing Qatar and other traditional LNG exporters.

The U.S. Department of Energy (Doe), in a communiquépublished on March 16th, announced that his country had become the world’s top LNG exporter. In the same statement, the DOE reported that this year an additional capacity on current volumes would increase exports by 20 % by 2022, about 70 million cubic meters (MMCM).

According to data from the European Commission, the increase in US LNG supply to the E.U. has been progressive, from 16 % in 2019 to 44 % in January 2022, accounting for 75 % of its exports and making it the main supplier of LNG to the European market.

In January 2022, 74 % of the regasification capacity in the E.U. was used, which is currently at 13.5 billion cubic metres (BCM) per month, consisting of 21 operating terminals (9 of them with expansion plans), while two terminals are under construction and 11 are under planning.

Of course, it is necessary to clarify that the volume of gas transported via pipelines to Europe is much higher and at a lower cost, meeting 79.5 % of demand, while gas transported via LNG to Europe is much smaller and more costly meeting only 20.5 % of its needs.

Gas imports from Europe in 2021, via pipelines from Russia and other countries, totalled 320 BCM per year; total LNG imports into Europe, the U.S., Qatar and other countries totalised 64 BCMs per year (excluding 16 BCMs from Russia). That is, at the moment, gas imports from Europe are primarily via pipelines and, for the most part, come from Russia (38.3 %, including Russian LNG); to fully replace it — as announced — the production and export of LNG to Europe must reach 153 BCM (summing LNG exports from Russia), i.e. an increase of 140 %.

These volumetric and cost differences between the different sources and modes of supply not only pose a great challenge and risk in terms of the availability of gas and the development of infrastructure, both regasification, transport and liquefaction of Liquefied Natural Gas (LNG) but also implies an over-cost to the European energy matrix, which affects the competitiveness of the bloc.

The President of the European Commission (E.C.), Ursula von der Leyen, has been presenting alternatives to replace the Russian gas supply, which accounts for 36 % of the total gas consumption in the European Union; the most ambitious presented so far agrees on a guarantee to purchase U.S. gas, via LNG, of an additional 50 billion cubic meters per year.

The agreement signed on March 25th in Brussels by U.S. President Joe Biden and von der Leyen has strong political content but lacks the elements of a plan. The elaboration of this has been delegated to the private companies involved in the agreement. However, there is no information regarding existing capacities, development, infrastructure development, required resources, costs, execution time, and gas sales prices.

However, this plan or announcement to import 50 BCMs of LNG gas, additional to the 48 BCM planned for this year (12 BCM for the first quarter), would give a volume of 98 BCM of gas per year from the U.S., resulting in a 104 % increase over the expected volume for this 2022.

However, this extraordinary target, with no infrastructure forecast or LNG handling capacity, represents only 65 % of the 153 BCMs Russia supplies to Europe annually (including shipments to the E.U. via Turkey by the Turk Stream).

In other words, if successfully realised in an undetermined time and cost, the announced plan would still leave a volume of 55 BCMs of Russian gas that would not be replaced.

PRICES

OIL

The crude markers continued upwards. On June 3rd Brent (ICE) and WTI (NYMEX) were quoted at $119.7 and $118.8 a barrel, an increase of 22 % and 27 %, respectively, compared to the start of the war, impacted by the E.U.’s decision to block the supply of Russian oil to Europe and the uncertainty about oil supply, which on May 30th, soared prices to 123 dollars a barrel.

BRENT AND WTI QUOTES (January — June 2022)

SOURCE: Investing, Nymex, ICE.

Throughout May, prices have remained above $100 a barrel, fluctuating between $105-114 a barrel until May 25th, then standing above $120 on 30 and 31 May.

While it is true that oil prices reflect a sustained upward trend since the second half of 2021, to stand at $80 a barrel, resulting from the recovery of the market, since the beginning of February, prices reflect a “war premium” of about $40 per barrel for the Russian invasion of Ukraine.

This price band could move to a level between $110-120 a barrel as a result of the E.U.’s decision to block the supply of Russian oil to Europe and the problems faced by E.U. countries in replacing the supply of 4.1 million barrels per day of oil and Russian products, while other producer countries grouped in OPEC+. Despite agreeing to accelerate their policy of flexibilisation and produce 640 thousand barrels per day between July and August, they have struggled to reach previously agreed production levels.

Only the U.S. has been increasing its oil production capacity continuously, 600 thousand barrels per day since the beginning of the year, sustained by the price levels and producers of shale oil, which have brought U.S. production to 11.9 million barrels per day, which has allowed the U.S., although its oil exports remain at 3.3 million barrels per day, the same values since the beginning of the year.

The market perceives that the oil supply is declining, both for political and economic reasons. There are no capacities either to replace Russian oil or to meet current demand and projections towards the end of the year. Therefore, the U.S. and IEA have had to resort to the release of Strategic Petroleum Reserves (SPRs), despite the price remaining at high levels, boosting inflationary phenomena and rising prices, which is a brake on the recovery of the world economy.

Prices will continue to react upwards as, in a market with no additional oil production capacities, political decisions to block supply and economic sanctions affecting two of the largest oil producers are intensified or maintained: Russia and Iran.

GAS

Gas prices in Europe have been quoted upwards since mid-2021, both due to the recovery of the economy and rising demand from the continent’s industrialised economies, restrictions on transport capacities and the low level of available gas storage. All of the above are associated with the effects of COVID during 2020-2021.

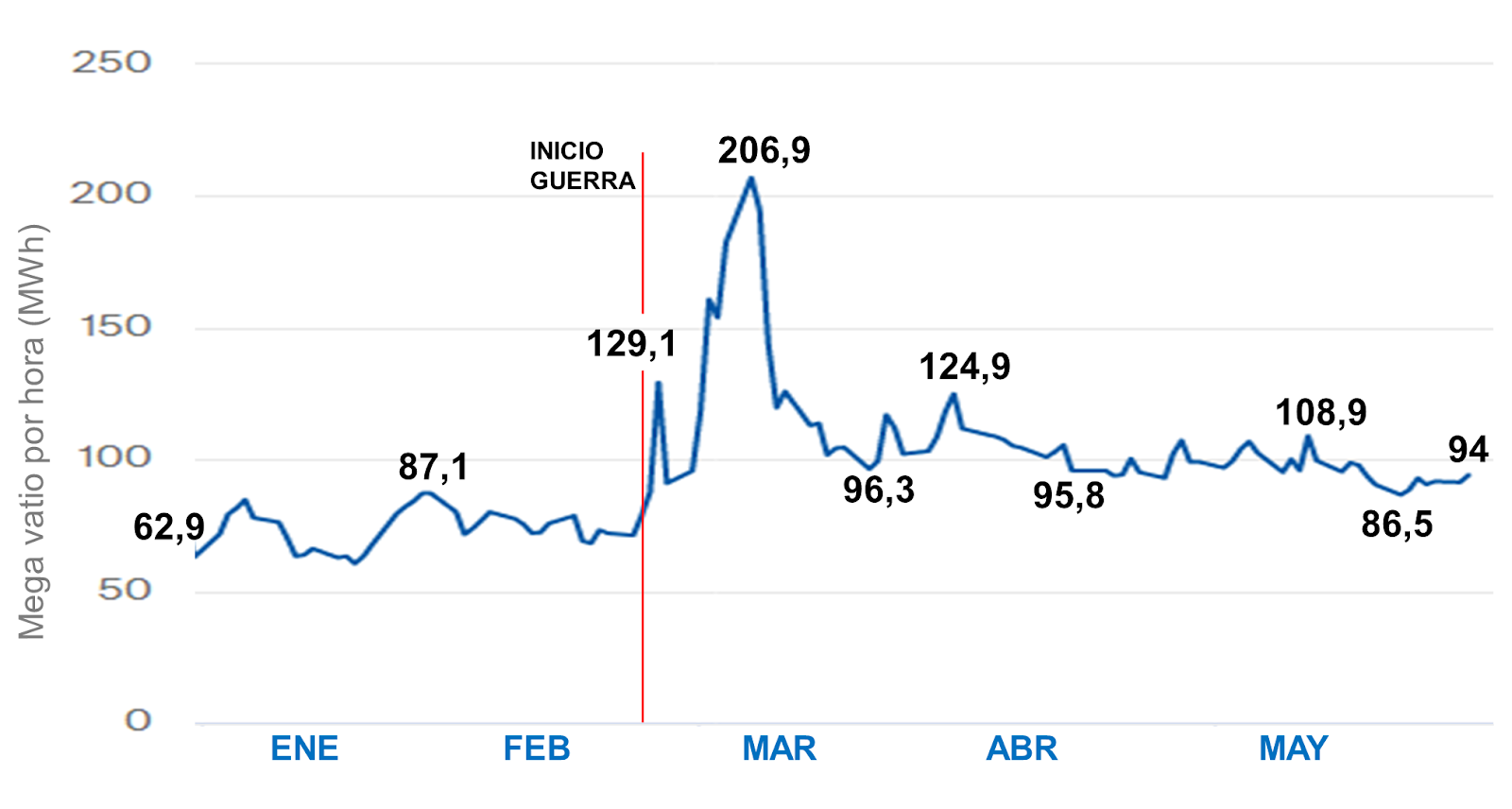

However, starting with the Russian military intervention in Ukraine, on February 24th, the price of Dutch TTF Future Gas, the gas scoreboard for Europe, soared by between 80 and 130 %, to stand at record prices of EUR 207/MWh at the close of March 7th.

As of April 15th, the price of Dutch TTF Gas Futures, the benchmark for the value of gas in Europe, moves around EUR 95 per megawatt-hour (MWh), with a band fluctuating between EUR 80 and EUR 110, MWh, well below the March prices between EUR 100 and EUR 300 per MWh.

Since May 20th, gas in Europe has been trading between EUR 86 and EUR 94 on MWh (still 650 % above the pre-COVID values) due to the seasonal change and the gas supply Europe has been receiving, both by pipeline and LNG, which has allowed gas reserves to rise to 44 % of its capacity, 10 points more than last year.

GAS PRICE IN EUROPE January — May 2022

Source: own production with Intercontinental Exchange (ICE) image and data

One element that has made it possible to stabilise the gas price in Europe downwards is that the gas supply has not stopped, maintaining the supply according to the volumes contracted. From the Russian government, through Gazprom, it has been reported that gas supplies to Europe have been maintained since the beginning of the conflict.

In March, 109 million cubic meters (MMCM) of gas were transported per day, the maximum capacity of the pipelines crossing Ukrainian territory. In April, it dropped to 48 MMCM by the end of the month.

In May, at the beginning of the month, the supply rose again, to 95 MMCM, and then went down every week to 44 MMCM on May 23rd because Ukraine announced that it refused the entry of Russian gas by the Sokhranovka gas distribution station in information published by the Ukrainian Gas Transmission System (GTSOU), as it could not guarantee the operations due to the presence of Russian troops in the Donbas region, this affected the normal flow of gas. This action was nothing more than a way by Ukraine to put political pressure on Europe using the Russian gas blockade.

At the end of May 31st, gas prices in Europe marked EUR 94 MWh, with a downward trend, while supply remains uninterrupted from Russia; however, these values are still more than 60 % above gas prices in the second half of 2021.

ECONOMY

The conflict between Russia and Ukraine is causing a slowdown in the growth of the world economy, mainly due to cuts in the supply chains of primary and final goods, which also generates inflation. According to the IMF, global growth is projected to slow from 6.1 % in 2021 to 3.6 % by 2022 and 2023.

Fuel and food prices have risen rapidly, particularly affecting vulnerable populations in low-income countries.

Increases in commodities and pressures on intermediate and final goods prices have led to inflation projections for 2022 of 5.7 per cent in advanced economies and 8.7 per cent in emerging and developing market economies.

In the case of Russia and Ukraine, the IMF projected that their gross domestic products would contract respectively by 8.5 % and 35 %.

In this way, the global recovery that had begun following the withdrawal of COVID-19 in the major developed and emerging economies is changing again, with the aggregate of inflation; this phenomenon, which was not observed during the months of the pandemic, aggravates an already complex international landscape for an indeterminate time.

Inflation and energy

According to the Organisation for Economic Development Cooperation (OECD) Consumer Price Index, issued May 4th 2022, by March this year, annualised inflation in their economies would have increased by 8.8 %, while energy prices increased by 33.7 %, both compared to 2021.

By country, inflation and energy varied, respectively, for the United States, 8.5 % and 32.0 %; Germany, 7.3 % and 39.5 %; Canada, 6.7 % and 27.8 %; Italy, 6.5 % and 50.9 %; The United Kingdom, 6.2 % and 27.8 %; France 2.5 % and 29.5 %; and Japan, with 1.2 % and 20.8 %.

For its part, China, the largest Asian economy and the second-largest in the world presented April this year 2.1 % annual inflation in the Consumer Price Index (CPI), with a cumulative 1.4 % in 2022, where energy rose by 20 % in 2021, according to recent publications by the National Bureau of Statistics of China. During the second quarter of the year, China’s economy was affected by the COVID outbreak in key cities such as Beijing and Shanghai, which led to containment and confinement measures by the Chinese authorities in the framework of their “Zero COVID” policy.

According to the World Economic Outlook of the International Monetary Fund, its growth projections for April of this year — after two months of war — underwent a downward adjustment.

In its report, the IMF adjusted the growth of the U.S. economy to 3.7 %, 0.9 points lower than expected last October. Regarding the eurozone, growth was projected at 3.9 %, a decline of 0.4 percentage points. Meanwhile, the Chinese economy was projected at 4.4 %, a decrease of 0.4 percentage points compared to its previous estimates.

Inflation in the cost of raw materials and the difficulties generated in the food and energy supply chain, rising since the beginning of the war in Ukraine, accelerate inflation rates again in industrialised economies, bringing them to record levels.

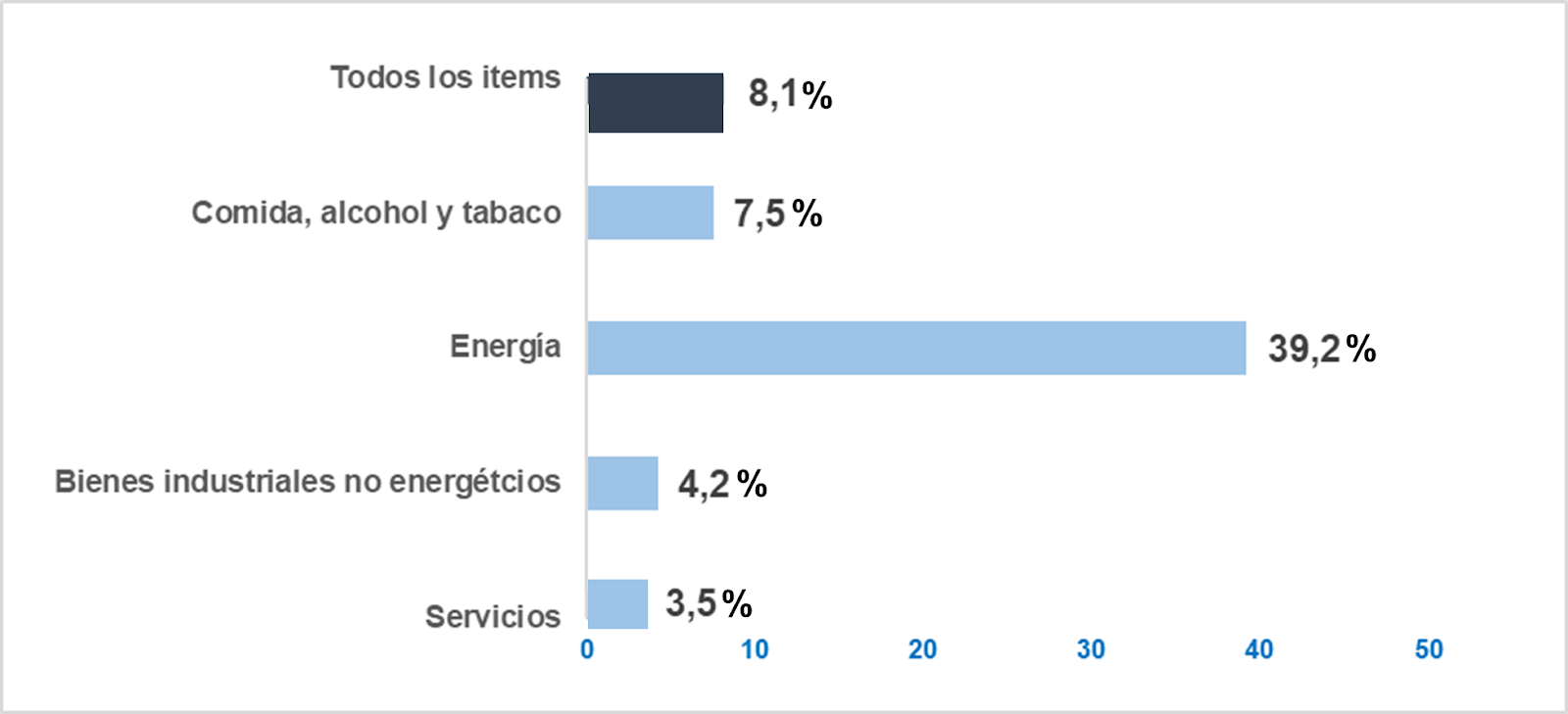

During April, the U.S. and the European Union (E.U.) economies maintained high annual inflation rates. The annual inflation rate in the E.U. for April recorded a record 8.1 %, Eurostatreported on May 18th, the highest in its history, increasing 0.3 points over the previous month, leading the European Central Bank (ECB) to advance the increase in the interest rate, according to its president, Christine Lagarde.

It is important to note that energy price inflation in Europe recorded an annual rate of 37.5 %, which still does not consider the sanction’s impact on the supply of Russian oil and fuels to Europe.

Annual inflation rate in the euro area (May 2022)

Source: Bloomberg

For its part, since March, the U.S. has had the highest annual inflation rates in more than 40 years, surpassing 8 % (8.5 % in March and 8.3 % in April), an annual rate of inflation that was not recorded since 1981, at the end of the “Great Inflation” crisis. On May 4th, the U.S. Federal Reserve (EDF) increased the interest rate in federal funds by 0.5 points, bringing it to 1 %.

The annual rate of energy inflation in the U.S. was 30.3 %, and that of gasoline was 43 %, according to the latest report presented by the U.S. Bureau of Labor Statistics on May 11th.

Rising fuel prices in the U.S. have reached average prices of up to $4.6 a gallon (in California, it reached $5.84 a gallon), keep occurring despite repeated calls by president Biden to companies to curb prices in the domestic market, something that has not happened. In addition, oil companies and the U.S. refining sector have been performing with large profits and margins.

“Ceiling” at the price of energy in Europe?

Energy companies have made extraordinary gains at this juncture in rising oil and gas prices, with rising fuel prices in their own countries’ domestic markets causing inflation to rise.

The most important companies in Europe and the U.S. have shown extraordinary profits in the first quarter, while the economy falls and energy inflation increases in their respective countries. A contradictory situation that reflects a lack of control and regulation by the State, as these are strategic issues for the countries’ economies.

High oil and gas prices and rising demand will cause major oil corporations to break record cash flow by 2022. Norwegian researcher company Rystad Energy estimates that it exceeds $830 billion – 70 % above the $493 billion recorded in 2021. Among the corporations, ExxonMobil stands out, presenting the most significant increase in the year, at 18 billion dollars. During the first quarter of the year (before counting the impact of the war), energy corporations had recorded the largest profits in their history for a quarterly period. ExxonMobil had adjusted profits of $8.8 billion, while Shell’s profits were $9.13 billion, ENI’s $3.8 billion and Repsol was $1.1 billion.

In response to this situation in Italy, Prime Minister Mario Draghi earlier last month proposed to the E.U. Parliament to “establish a ceiling” to the price of energy in Europe, intervening in the market and regulating the excessive profits of companies in the sector to protect consumer income, curb inflation and prevent a further fall in the economy.

This measure was already partially taken in Italy, where last March, a reduction of € 25 cents per litre was established in the price of gasoline, initially for 30 days, now extended until July 8th. However, it has not been enough to contain inflation.

This measure — which has begun to be assessed by the E.U. — will have to go through a lengthy negotiation process to subordinate business interests to those of countries’ politics and economy, even more so in a context following the Russian oil blockade, which further restricts and increases the supply of energy in Europe.

European companies accept payment in rubles

On March 31st, President Vladimir Putin instructed the Russian gas state-owned Gazprom to bill Russian gas purchases in rubles to counter the effect that sanctions have had on the Russian economy and currency, avoiding a further devaluation of the ruble.

Among the first sanctions packages adopted against Russia by both the U.S. and the E.U., 600 trillion dollars of the reserves of the Russian central bank were frozen in European banks, which was immediately reflected in the depreciation of the ruble and the possibility of Russia falling into default with its debt holders.

However, the Russian economy has resisted more than expected analysts, holding the ruble’s value, while it has not ceased its debt payments, so it has not fallen into default. Undoubtedly, revenues from gas and oil sales have been one of the fundamental factors that have prevented the collapse of the Russian economy. In contrast, Moscow’s new willingness to receive gas export revenues to Europe in rubles is a measure that underpins the value of its currency in the face of an extraordinary situation.

Most European companies have migrated to the payment scheme demanded by Gazprom, even though there is strong political pressure not to accept the new modality, companies and countries that rely on Russian gas supply are not willing to do anything that causes the interruption of gas, especially when there is no explicit E.U. ban on this type of operation, as clarified by European Commissioner for the Economy, Paolo Gentilone.

On May 17th, the Italian ENI announced that it had opened both accounts at Gazprombank to pay for Russian gas purchases. According to the Italian company, the transaction “should not be incompatible” with the sanctions imposed by the E.C. on Russian banks and the Central Bank of Russia. ENI became the first company to commercialise Russian hydrocarbons to adapt to the payment method imposed by Gazprom. Several governments are willing to comply with Gazprom’s demands, as announced on April 27th by the government of Hungarian President Viktor Orban,announcing that his country accepted the payment conditions imposed by Gazprom.

From the end of April, Russia began to take action against countries that refused to pay for the supply in rubles under the conditions imposed on March 31st.

On April 27th, Gazprom stopped supplying gas to Poland, Bulgaria and Finland, countries that have refused to accept payment in rubles and have maintained a rather hostile policy towards Russia since the beginning of the conflict.

Almost a month later, on May 21st, Gazprom suspended the supply of gas to the Finnish company Gasum, affecting more than 90 % of the gas imported by Finland. On May 31st, the Netherlands ceased receiving gas supplies from Russia after the Dutch company, GasTerra (50 % state-owned), refused to pay the supply contracts in rubles, which, due to the duration of the contract (October 1st 2022), could result in the loss of 2 BCM of agreed gas.

On June 1st, it was the Danish companyOrestedthat stopped receiving Russian gas, affecting two-thirds of the gas in Denmark; it also occurred with Shell Europe, affecting 1.5 % of Russian gas imports into Germany.

Amid the suspensions to the companies that refused to pay in rubles, on May 12th Gazprom announced that, as a measure against E.U. companies, it imposed sanctions on Europol GAZS.A., owner of the branch of the Yamal-Europe pipeline that passes through Poland, suspending the shipment of gas through the branch mentioned above.

OIL DEMAND

At the beginning of 2022, both OPEC and the agencies estimated that global oil demand would be above the 100 million barrels-day barrier, a historical level that reflected the recovery of the post-COVID world economy, with an estimated growth suspending 4.2 points for this year.

Thus, OPEC estimated in January that the world demand for oil would be 100,9 million barrels per day, while the IEA and the EIA did so at 100.6 million barrels per day of oil, coinciding with their forecasts.

However, after the onset of the war, high oil prices and the decline in economic recovery, global oil demand has declined in its growth estimates, although it remains at historical peaks, above 2019 levels before COVID-19.

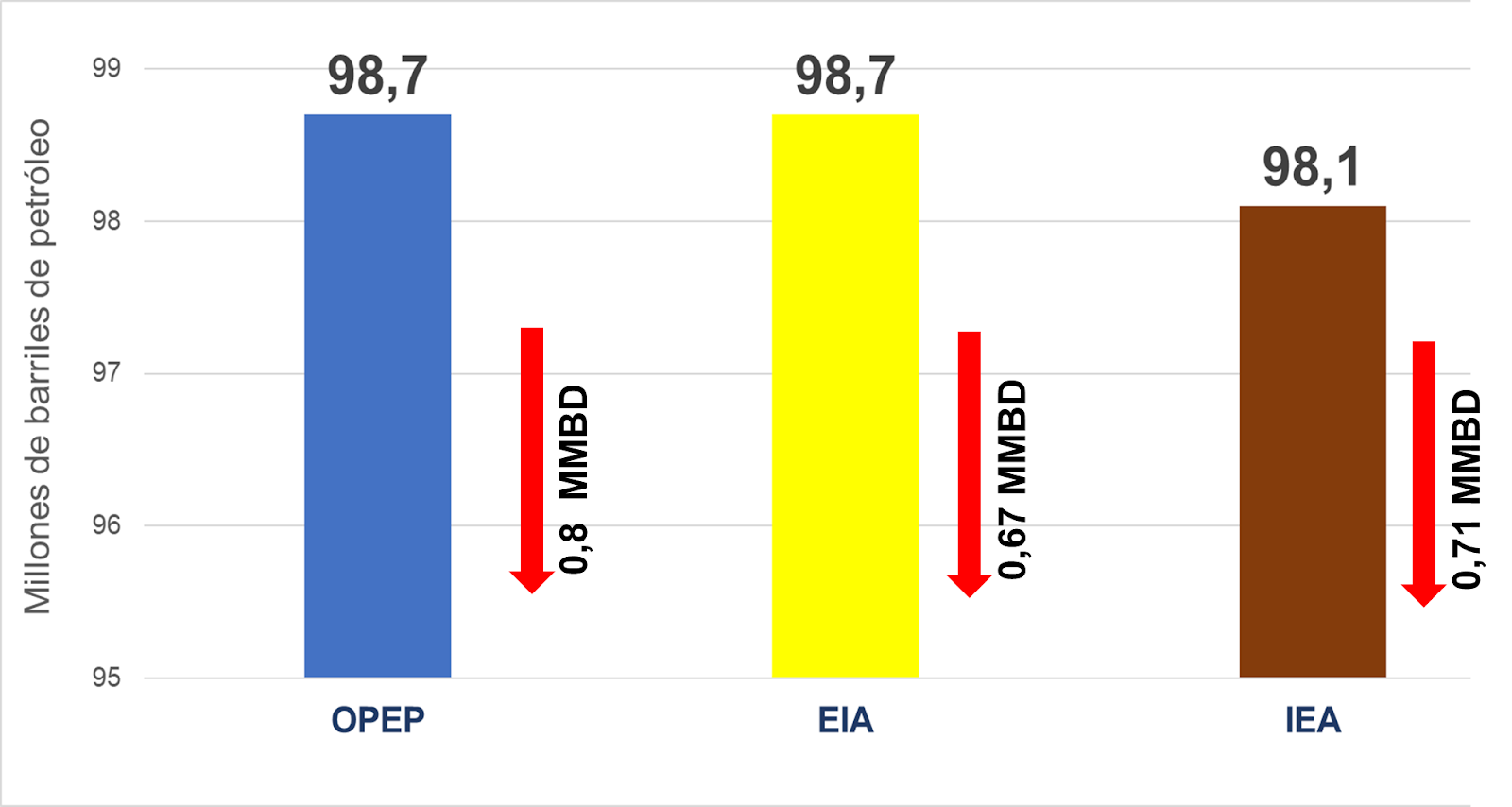

Thus, in its May MOMR, OPEC estimates that global oil demand will be 100.3 million barrels per day, a reduction of 600 thousand barrels per day compared to its year-on-year estimates.

In its monthly report of May 10th, the EIA adjusted by 1 million barrels per day to its downwards projection of demand for this year, remaining at 99.6 million barrels per day. While the IEA, in its May report, projects demand for 2022 at 99.4 million barrels per day, representing a downward adjustment of 1.2 thousand barrels per day from its pre-war estimates.

DEMAND ESTIMATION (2022)

Source: Own production with OPEC, IEA and EIA data.

Despite geopolitical tensions and uncertainties surrounding the oil economy and market, projections on global oil demand remain at robust, historical levels, indicating that in the face of fears and risks surrounding oil supply, the fall in oil production capacities, whether due to lack of investment and economic problems, affecting producers in Africa and Latin America, the war in Ukraine, as well as the embargo and sanctions imposed on Iran and Russia, the price will continue to rise or remain stable in a band, consistently above $100 or 110 dollars per barrel.

It is clear that, since the beginning of the year, following the post-COVID economic recovery, there has been unsatisfied demand, which has pushed up prices since mid-2021, not only for oil but for gas and coal. Fossil energies, which still account for 83 % of the world’s energy matrix, continue to rank first as engines of the world’s economy.

The war in Ukraine and the embargo on Russian oil reinforce the upward trend in prices by placing supply risks in an oil market with high oil demand.

OIL PRODUCTION

Petroleum, liquids and condensates (PLC)

According to OPEC data in its May 12th monthly report(MOMR), world production of oil, liquids and condensates, as of April, stood at 98.7 million barrels per day, showing a monthly decrease of 800 thousand barrels per day.

Other sources, such as the EIA and IEA, reported that worldwide PLC production for April was 98.7 million barrels per day and 98.1 million barrels per day, respectively, with a monthly drop of 670 thousand barrels per day and 710 thousand barrels per day.

WORLD PRODUCTION

raw, condensed, LNG and unconventional (April 2022)

Source: own elaboration with data from the MOMR OPEC of May 12th, STEO report of the IEA of May 12th and monthly report of the EIA of May 10th.

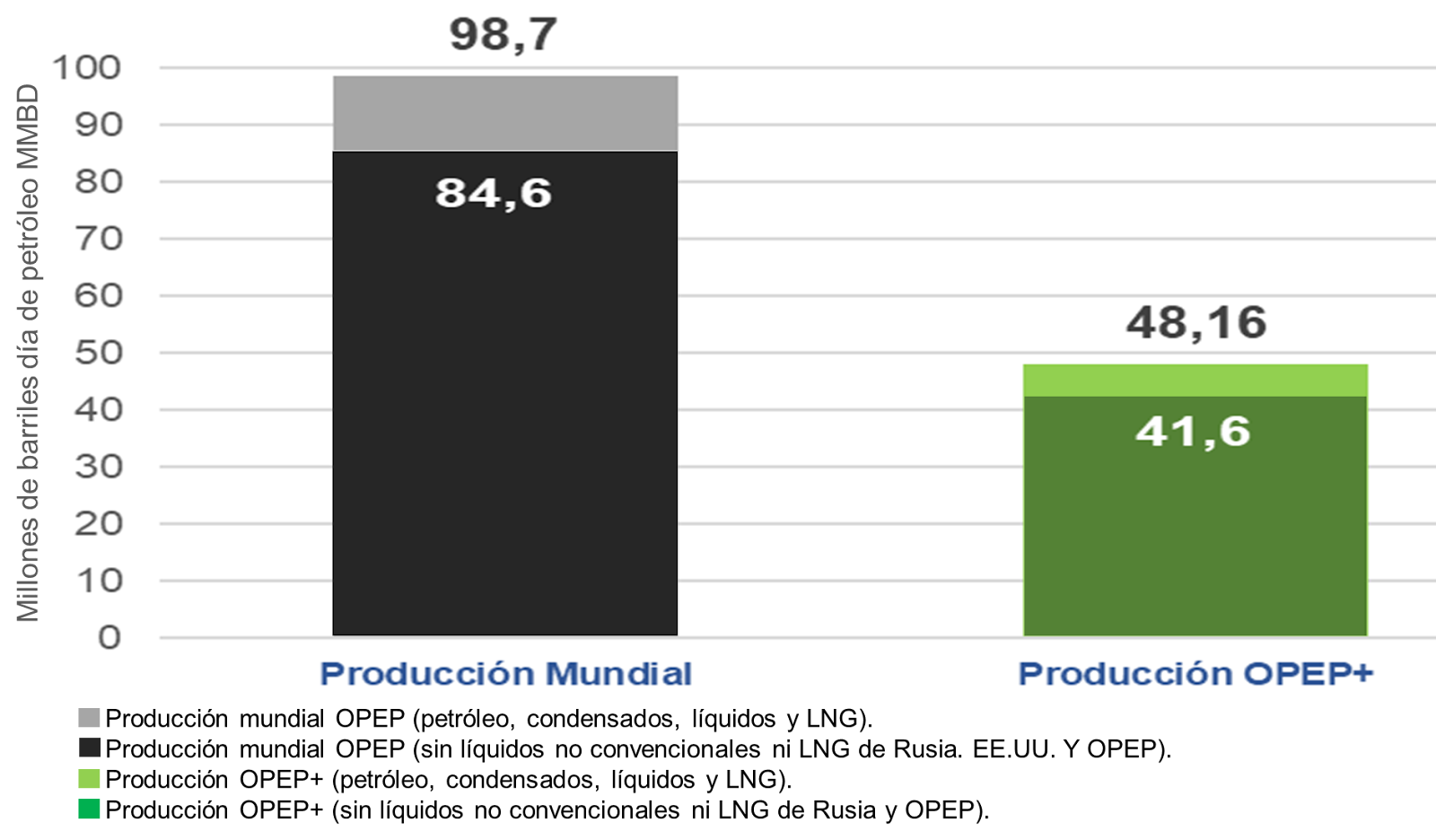

World oil production

World oil production in April 2022 stood at 84.6 million barrels per day, a 1.6 million barrels per day drop from oil production in March, mainly as a result of geopolitical factors affecting Russian production (930 thousand barrels per day), Libya (160 thousand barrels per day) and Kazakhstan (150 thousand barrels per day).

WORLD OIL PRODUCTION (April 2022)

Source: own production with OPEC, AIE and Argus Media data.

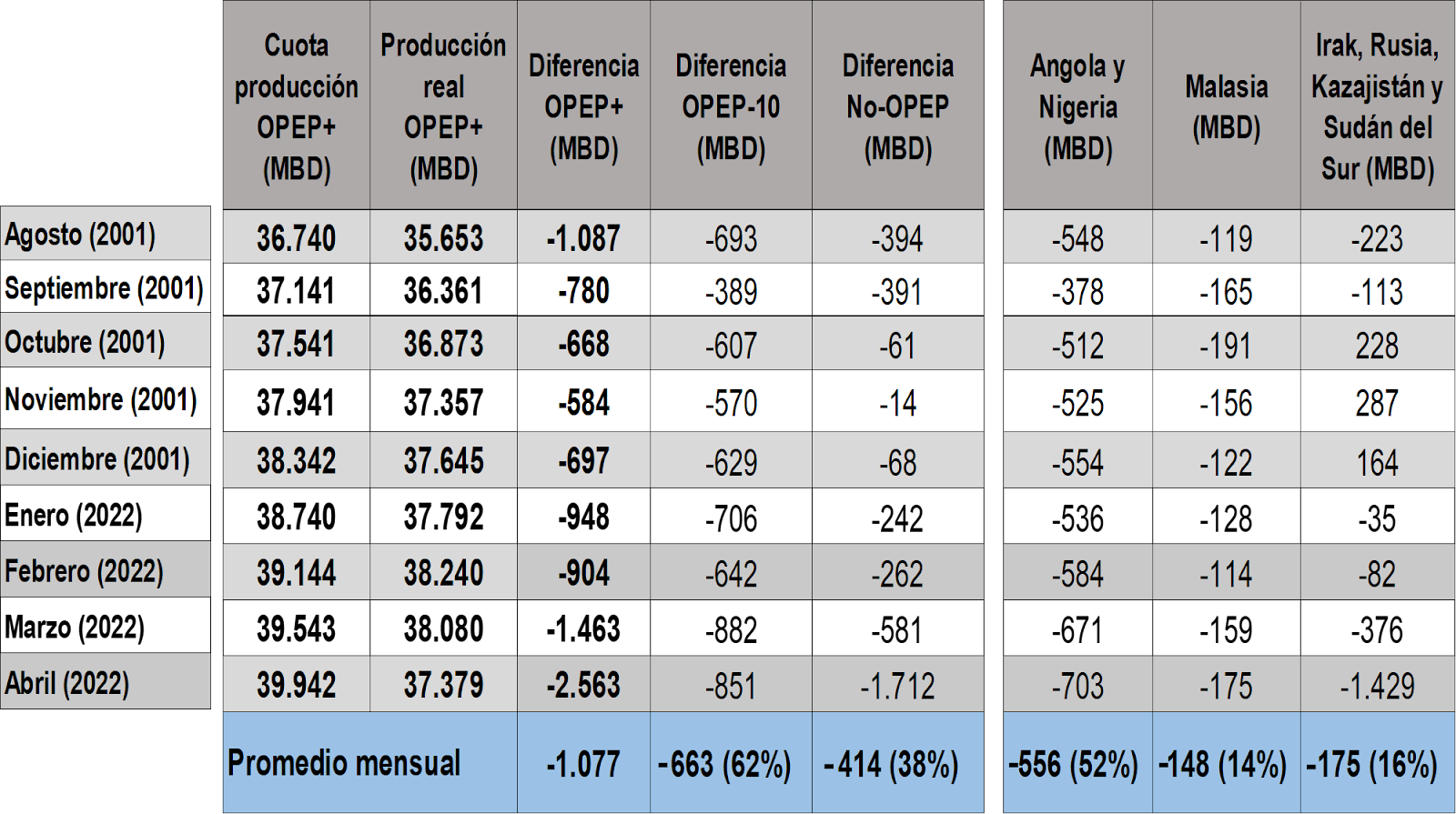

Of the world oil production of 84.6 million barrels per day, 41.6 million barrels per day (49.2 %) corresponds to the production of OPEC+ countries.

From August 2020 to April 2022, OPEC+ has increased its share of oil production by 7.54 million barrels per day, with an effective increase in crude oil supply of 6.1 million barrels per day.

From the initial cut of 9.7 million barrels per day in May 2020, 2.16 million barrels per day remains due to return to the group’s production quotas; according to the decision of the last OPEC+ meeting on June 2nd, with an increase in its flexibility quota from 200 thousand barrels per day to 640 thousand barrels per day by July-August, the production cut will have ended on August 31st. Thus, OPEC+ decided to de facto advance the end date of the cuts, initially scheduled for December 31st.

OPEC+ production

By April 2022, OPEC+ production, including Iran, Libya and Venezuela (with no cuts), had a monthly drop of 800 thousand barrels per day and stood at 41.6 million barrels per day, despite an increase of 400 thousand barrels per day in its production quota for the month.

The decline in OPEC+ supply corresponds to a drop in production in Russia (930 million barrels per day), Kazakhstan (150 thousand barrels per day) and Libya (160 thousand barrels per day), together with the production problems that Angola, Nigeria and Malaysia have been facing to reach their production quota in the month.

Since the OPEC+ production quota adjustment mechanism (400 thousand barrels per day per month) began in July 2021, the group could not reach the production quota allocated to it each month, where actual OPEC+ production has ceased to produce an additional 1.08 thousand barrels per day average over the past nine months. This shows that the market is well stocked, without the need for extra production capacity.

VOLUME OF NON-COMPLIANCE OPEC+ QUOTAS (August 2021 — April 2022)

Source: own production with data from the OPEC MOMR of May 2022, the Ministry of Energy of Russia and Argus Media.

While it is true that before the start of the war in Ukraine, the volumes of OPEC+ were already below its monthly production quota, the sanctions imposed on Russia have led to a fall in Russian production and the countries in the Caspian Sea, in particular Kazakhstan, due to the cancellation of the scheduled oil charges at the Russian oil terminal in Novorossiysk, 200 kilometres from Mariupol, Ukraine, which was reflected above all in April.

On the other hand, Nigeria maintains its problems in restoring its production levels amid the vandalism of pipelines and the lack of capacity to repair and maintain them, where Nigeria’s Upstream Petroleum Regulatory Commission estimates that the country’s actual production is 1.5 million barrels per day, but loses an average of 115 thousand barrels per day of oil by vandalising pipelinessince January 2021.

In the case of Angola, on May 12th, the country’s Minister of Mineral Resources, Petroleum and Gas, Diamantino Azevedo, said that with the changes made to the legislation, the tendering of new blocks was re-initiated, with projects scheduled to start offshore production activities in 2023, which allows to increase and stabilise their oil production, to reverse the fall in production that caused the lack of investment in recent years.

For its part, Libya’s production was affected by the blockade of the oil fields and ports to the east of the country, on April 17th, by the Libyan National Army (ENL) and the Eastern Parliament, which caused a fall in the country’s production of 160 thousand barrels per day that lasted four weeks, when the parties reached an agreement for the release, an episode that demonstrates the high degree of political instability that still affects Libya and its oil and gas production.

New production quotas in OPEC+

April will be the last month where OPEC+ countries that cut their production (except for Iran, Libya and Venezuela) will measure their quota under the current production benchmark of 42.1 million barrels per day.

From May, the production benchmark will rise by 1,632 million barrels per day and will remain at 43,732 million barrels per day, where only five countries will increase their quota: Saudi Arabia, UAE, Iraq, Kuwait and Russia; however, it is expected that Russia will now have trouble reaching its new OPEC+ production quota with the U.S. and Europe’s economic sanctions.

This new distribution of quotas from which most OPEC+ countries have been excluded demonstrates the fragility of supply and the lack of additional oil production capacity among the countries participating in the agreement.

There is no additional oil production capacity in OPEC+ countries to replace Russia’s volumetrics in the short term, and it is even to be seen whether the group can reach its new production base of 43,732 million barrels per day of oil by June.

OPEC production

According to the May OPEC Market Monitoring Report(MOMR), oil production from the 13 member countries as of April 2022, was 28,648 million barrels per day.

PRODUCTION OF OPEC COUNTRIES (April 2022)

Note 1 On March 31st, OPEC took the decision not to continue using IEA data, which it accuses of “lack of independence” and being “biased” towards the U.S., which creates a “technical problem” in the evaluation of the market and its data.

Source: OPEC MOMRof May 12th 2022.

In April, OPEC production rose monthly by 153 million barrels per day, despite the fall of 161 thousand barrels per day in Libya’s production, indicating that the fall in OPEC+ production occurs mainly in the non-OPEC countries that are signatories to the DoC agreement.

71.3 % of OPEC production (20,428 million barrels per day) is concentrated in the Persian Gulf countries (without Iran); whereas 14.1 % (4,036 million barrels per day) in African countries (without Libya); the three countries free from production cuts (Iran, Libya and Venezuela) accounted for 14.6 % (4,184 million barrels per day), of which 63.4 % are Iran and 21.8 % are Libya.

Russia, the great unknown

The massive economic and financial sanctions imposed on Russia caused — for the first time since the beginning of the war — a significant drop of 930 thousand barrels per day in Russian oil exports last April.

This drop of 9 % in Russian production and 22 % in OPEC+ was the critical factor in the fall in the group’s production in April.

RUSSIA’S OIL PRODUCTION (January 2020-April 2022)

Source: Own production with data from OPEC’s MOMR.

After reflecting on the fall in Russian production in April, the Russian authorities, through the Russian Deputy Prime Minister and Minister of Energy and Gas, Alexander Novak, in a statement on May 9th, have reported that the situation has been resolved. During May, production levels in the country were restored to pre-war levels, i.e. 10 million barrels of oil per day.

However, OPEC made forecasts in its production projection for the rest of the year that Russian production will not recover the level presented in the first quarter of the year and average of 9.5 million barrels per day during the second half of 2022, i.e. a drop of 500 thousand barrels per day.

The situation of Russian oil production and export resulting from the war in Ukraine and the massive sanctions imposed on the country is currently one of the most important elements in predicting the behaviour of the oil market, the big unknown.

With Russia being the second-largest oil exporter globally, the possibility that its production levels will collapse or be significantly affected by war or sanctions keeps the “premium” of war on the market, with prices above $100 a barrel. If Russia’s oil production collapsed in the short term, the price would soar, as there was not enough oil supply to meet current demand.

Given the situation of political criticism and propaganda, information and estimates regarding the reality of Russia’s oil production have become a vital issue for war and the economy due to the possibility for Russia to sustain its military and oil performance amid the heavy sanctions imposed by the U.S. and the E.U.

Therefore, the estimates made in this regard must be carefully observed and verified with independent sources, all of which add an important uncertainty factor to the market.

Thus, as soon as the war began, the Oxford Institute predicted the possibility that Russian production would fall in 4 million barrels per day in the event of a collapse of the Russian economy, similar to that suffered in the 1990s after the fall of the Soviet Union. For its part, the IEA predicted in its March reportthat Russian oil production would fall by 3 million barrels starting in April.

The actual situation of Russian oil production and industry remains unknown to the Western market and intelligence and strategic analysts.

What happened in April is most likely related to Russia’s difficulties in exporting and placing its oil volumes with its traditional and European customers rather than to problems arising from its short-term production capacities.

Since Russia invaded Ukraine, there has been strong political pressure among market operators, especially in Europe, not to commercialise Russian oil due to political sensitivities and pressure from public opinion against Russia.

Large oil companies have assumed relations with Russia as a “reputational” problem for their companies, affecting the commercialisation of crude oil and Russian products in Europe and other markets. Major European operators in the sector such as BP, ENI, Repsol and Galp have suspended all their oil operations with Russia; while Shell, Total and Glencore maintain the contracts already signed, they will not perform any new contracts with Russia.

The commercialisation of crude oil and products from Russia has faced problems with chartering and safe oil vessels due to the same political pressure on the market. Since the beginning of the war, Russian giant Rosneft, Lukoil and other operators have been forced to sell at discounts of up to 35 % oil and product shipmentsdue to the impossibility of translating them with their traditional customers in Europe.

The embargo on Russian oil imposed by the U.S. on March 8th, which affects 580 thousand barrels per day of Russian exports,is added to the embargo imposed by the E.U. on Russian oil on May 30th, affecting 4.1 million of its exports. There is a strong U.S. political lobby for its allies or major oil importers, such as India and other Asian economies, to stop buying oil and products from Russia as part of its goal of imposing a global “embargo” on Russian oil.

These measures represent a tremendous impact on the oil market, which has generated a frantic activity in trading and trading this significant amount of oil and product volumes required by the world economy, but whose trading is blocked for political reasons, is what has been called a process of “deglobalisation” for political reasons.

The market must wait for a period of transition, and refurbishment, where Russian oil volumes that are not purchased by the U.S. or Europe will necessarily be acquired by other major consumers, especially China, India and other economies that are making significant efforts to reactivate themselves after the devastating effects of COVID-19.

We say necessarily because there are no surplus oil production capacities on the market capable of replacing Russian production and because the oil demand is present there, at pre-COVID levels.

The oil market — unlike the gas market — is a mature, global market with great flexibility to adapt to disruptions in supplies, as it has already demonstrated in previous crises, such as the Arab embargo of 1973.

U.S.

The latest EIA weekly report, June 2nd, ranks U.S. production at 11.9 million barrels per day since May 9th, showing an increase of 300 thousand barrels per day from March and April and 600 thousand barrels per day from the beginning of the year.

Thus, the US remains the world’s largest oil producer, and its production is increasing, above the levels forecast in 2021 by the Department of Energy itself (DOE).

In the last 22 months, U.S. oil production has recovered 2.8 MMBDs from production, mainly due to Shale Oil production increase in the Permian Basin.

After the hydrocarbon sector began to recover losses and pay off debts and dividends from the first quarter of 2021 with the recovery of price levels, it seems that thanks to the stimuli given by the Biden administration, price levels above $100 a barrel and the political conjuncture for the war in Ukraine, the large U.S. energy corporations (ExxonMobil, Chevron and ConocoPiphills), like the producers, including the independent producers of Shale Oil, have concentrated mostly efforts and resources in the Permian Basin to bring U.S. production to 12.5 million barrels per day by the end of 2022, according to the monthly EIA report.

U.S. OIL PRODUCTION* (March 2020 — January 2022)

* Not condensed, LGN, or unconventional liquids

Source: Own production with data from the STEO of the EIA of May 10th 2022.

The volatility of the oil price in March, as an effect of the war in Ukraine, made the monthly growth of inflation over fuels (petrol 18 % and diesel 22 %) and energy raw material (18 %) the highest recorded since the last period of the “Great Inflation”, in 1981, bringing the average national price of gasoline to 4.22 and that of diesel to $5.11 a gallon, with the first time in history touching the $4 and 5 dollars, respectively, the value on which it has remained.

In May 2022, the domestic price of fuels in the United States was marketed at unrecorded values, where the gallon of regular gasoline, as of May 30th, stood at $4.62 and that of diesel over $5.54, although local production has been increasing to 11.9 million barrels per day.

Since October 2021, when the WTI, after seven years, was requoted above $80 a barrel, refining and distribution costs rose, according to the May 23rd EIA weekly price report, representing more than 30 % of the cost of U.S. gasoline, something that had not happened in previous times that the barrel price has been above $80.

In the case of diesel, refining became 40 % of the gallon price in March and April of this year, which had never happened, even with the barrel above 130 or 140 dollars, as happened in 2008.

In April, oil accounted for $2.5 of the cost of the gallon of fuel (petrol and diesel), which, according to EIA, corresponds to the value of the price of oil per month; therefore, the variable that increased the price of fuels to record values, was the refining and distribution costs, whose operators have enjoyed extraordinary profit margins.

Despite the cost of fuels and their inflationary effect, the country’s demand for fuels continues to increase.

Incentives to increase oil and gas production

As with the geopolitical objectives of the White House and the Pentagon in Europe and the conflict with Russia, as well as the very needs of the American economy, President Biden’s administration has postponed its “Green Deal” to openly stimulate fossil energies, oil and gas, to increase their production and export.

Given the sensitivity of the environmental issue, especially among the Democratic base that brought it to the White House, Biden’s government moved different strategies — some direct and some indirect — for U.S. energy corporations and independent producers to increase production.

The government has ceded more federal land for oil activity, responding to corporate requests, as a direct strategy to encourage increased local production, which Biden promised he would not do during his administration.

On April 15th, the White House announced the release of 580 thousand square kilometres of the Federal Lands,which will be tendered for lease for the exploration and production of hydrocarbons, which will charge a royalty rate of 18.75 %, which means a 50 % increase in the rate; this leased land, which accounts for 20 % of the federal land that energy corporations were demanding to be sold since last year.

Another measure — this indirect one — has been the repurchase of the volumes of strategic oil reserves (SPRs) released in order to intervene in order to reduce the price, but with the commitment and the need to be restored between 2023-2024, this measure stimulates local oil production, especially Shale Oil by giving a security and price horizon to investors and Coverage Funds that support this type of production.

On the other hand, the large corporations and producers of Shale Oil have significantly been favoured by sanctions and blockades on Russian production, oil and products, both because of the rise in prices and the large markets that these political decisions leave at the disposal of American production.

The same is true of the U.S. gas and LNG producers, who, based on the agreements signed with the E.U. and the imminence of blocking the Russian gas supply to Europe, open a whole market of 153 BCM gas in Europe to producers and exporters with prices and contracts conditioned by the political climate.

Release of Strategic Petroleum Reserves (SPR)

Since November last year, Joe Biden’s administration has announced the release of oil from US RPS, pushing for other OECD countries to accompany the decision to curb the rise in oil prices. Although large volumes were released, uncertainty and geopolitical factors have kept the price above $110 a barrel.

In November 2021, the U.S. decided to release 50 million barrels of RPS to the market; in January of this year, the U.S. Energy Secretariat authorised the release of another 13 million barrels. In February, the U.S. announced the release of 30 million barrels more, while in Aprilannounced another major release of SPR, this time for 180 million barrels (1 million barrels per day) in six months, of which 60.5 million are part of 120 million barrels of oil and oil products from emergency reserves that the IEA agreed to release its 31 member countries.

There are 273 million barrels that the U.S. will release from its SPRs. In contrast, among the other IEA countries, Japan will release 15 million barrels, South Korea 7 million, Germany 6.5 million, France 6 million, Italy 5 million, United Kingdom 4.5 million, Spain 4 million, the rest of the European countries 6.5 million, Turkey 3 million and 2 million the countries of Oceania.

After falling to 409 million barrels at the end of March, commercial reserves of crude oil in the U.S. have been recovering, standing at 414 million barrels on May 27th, after reaching 424 million on May 13th, the EIA reported in its June 2nd weekly report.

Meanwhile, the SPRs have been decreasing their volume, draining 46 million barrels since the beginning of the war, remaining at 526 million barrels on May 27th; since Biden’s first announcement to release SPRs in November 2021, 82 million barrels have been drained.

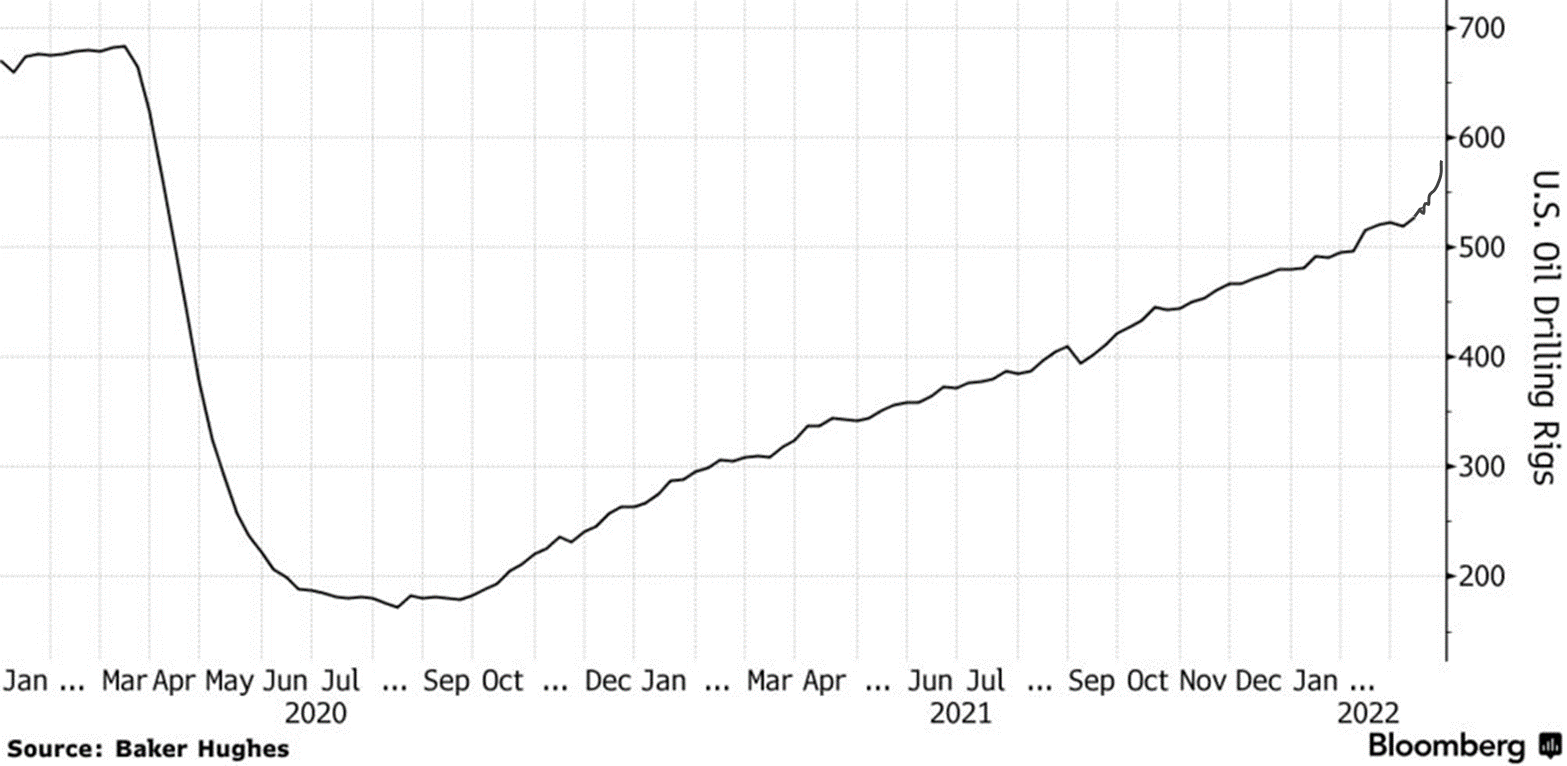

Drilling activity

The number of operating drills in the U.S. has risen by 20 % in 2022, from 481 to 574 at the end of May 20th, Baker Hughes reported on May 27th. Drilling operations in the Permian basin rose from 292 to 341, representing more than 59 per cent of the current active drills.

Between March and April, 1699 wells were drilled, and 1881 were completed, of which 182 DUC (Drilling but Uncompleted wells) started but were left abandoned, waiting for better prices — in the barrel of oil — to be completed. During the first four months of 2022, 3221 wells have been drilled, and 3719 have been completed, including 498 DUC.

ACTIVE DRILLS IN THE U.S. (January 2020 — May 2022)

Image: Bloomberg.

Active drills, as of May 20th, are 100 units below those recorded in the first quarter of 2020, before the outbreak of the pandemic; however, since October 2021, the number of operational drills has been at its highest record of activity since the outbreak of the pandemic, due to high oil barrel prices, where WTI has been trading at prices above $80 since mid-January 2022 and over $100 since the start of the war in Ukraine.

This shows that, during 2021, shale oil producers earned revenues that allowed them to recover losses and pay debts and dividends. Therefore, in 2022 they are in a financial situation and a price level that allows them to re-start and increase production.

OIL STORAGE

By April 2022, the OECD and U.S. trade inventories of oil and petroleum products showed a fall of 560 million barrels and 300 million barrels, respectively, compared to July 2020, to 2650 million barrels (OECD) and 1150 million barrels (USA).

TRADE INVENTORIES OF OIL AND PETROLEUM PRODUCTS IN OECD AND US COUNTRIES (January 2014 — May 2022)

Source: EIA.

By May 27th, the U.S. oil and petroleum products trade inventories (1155 million barrels), 151 million barrels below the last five years’ average. While according to OPEC’s latest MOMR, OECD trade inventories, as of March (2621 million barrels in March), were 300 million below the average of the last five years.

In the context of this complex situation of the oil market, Venezuela, a founding member of OPEC and which, until 2014, had an undisputed political leadership in the Organisation, with a specific market weight due to its production of 3 million barrels today, does not influence the Organisation, nor in the oil market.

The country’s grave political problems, production collapse since 2014, and international political isolation leave Venezuela out of any influence in the complex framework of current oil geopolitics.

OIL

Stagnant oil production.

The OPEC Oil Market Monitoring Report (MOMR) of May 12th put Venezuela’s oil production at 707 thousand barrels per day for April, indicating the stagnation of the country’s production around the same levels of 2019, which is 77 % below the production levels of 3,015 million barrels of oil day 2013.

OIL PRODUCTION OF VENEZUELA (April 2022)

Source: MOMR OPEC, May 2022

The OPEC report notes the levels of production, verified by the specialised agencies, from which the International Energy Agency (IEA) has already been excluded as having a significant political bias; this becomes — given the absence of oil control mechanisms in the country, or verifiable information in the country — the only Source to monitor the oil production situation in the country.

In other words, the best available information from the specialised sources of the international oil market used by OPEC belies the Venezuelan government’s announcements of an “extraordinary recovery” of oil production in the country.

The numbers and information of the international agencies available indicate that the information and projections issued by both the Oil Minister Tareck El-Aissami and Nicolás Maduro himself, ensuring that the country’s production is above one million barrels of oil and that it will reach the figure of two million barrels a day before the end of this year, are false, only government propaganda. The reality is that the Venezuelan oil industry is going through the worst crisis in its centuries-old history.

Current production levels of 707 thousand barrels per day include the volumes of diluents and crudes supplied by Iran to Venezuela, which are sold mixed with Venezuelan crude; as well as the volumes of water that are not separated by the problems of the oil treatment and conditioning infrastructure, which has led to claims and returns of oil shipments from the country.

Real levels of oil production are masked when mixed with Iranian crude, demonstrating the government’s inability to increase oil production and the oil industry’s collapse between 2015-2022, when the country’s oil production has fallen by 2,31 million barrels per day.

The current levels of oil production are equivalent to the country’s production levels in 1930, despite the fact that Venezuela has the largest reserves in the world, certified in 2007 and at 316 billion barrels of oil.

Oil collapse as a result of the disassembly of the policy of Plena Sovereignty Petrolera

Last Saturday, May 14th, the 1st Meeting of the Possible Country was held, with the oil theme: From the Petroleum Sovereignty to the Madurist Collapse.

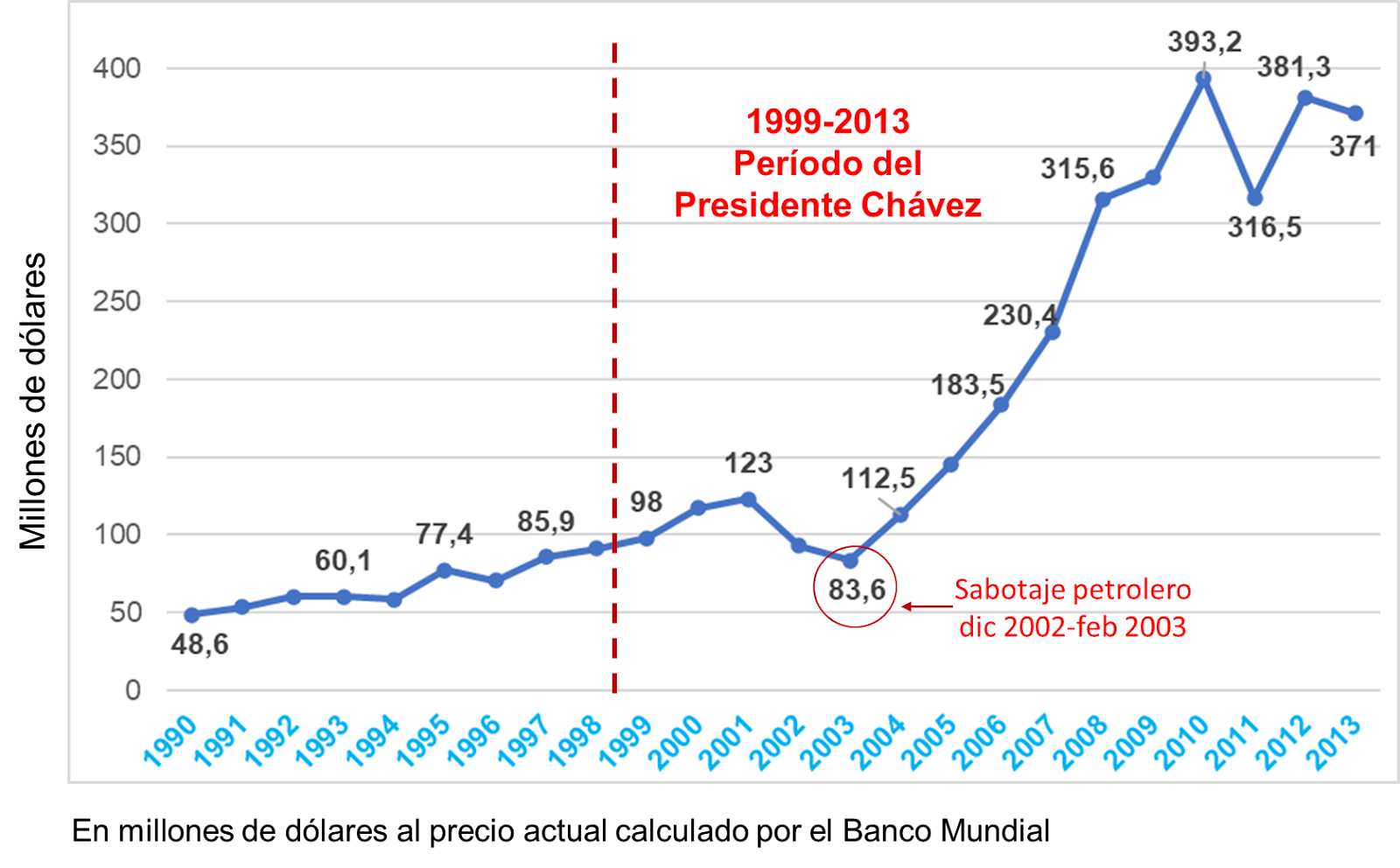

Here was an extensive exhibition where a review of the fundamental aspects of the Petroleum Sovereignty Policy in force in the period 2004-2014, during the government of President Chávez, which constituted the doctrinal basis and guide of the oil industry and PDVSA in particular, which lived stellar moments in this period, once restored its full operational capacity severely affected by the oil sabotage suffered by the industry between 2002-2003.

OIL PRODUCTION VENEZUELA (1999-2014)

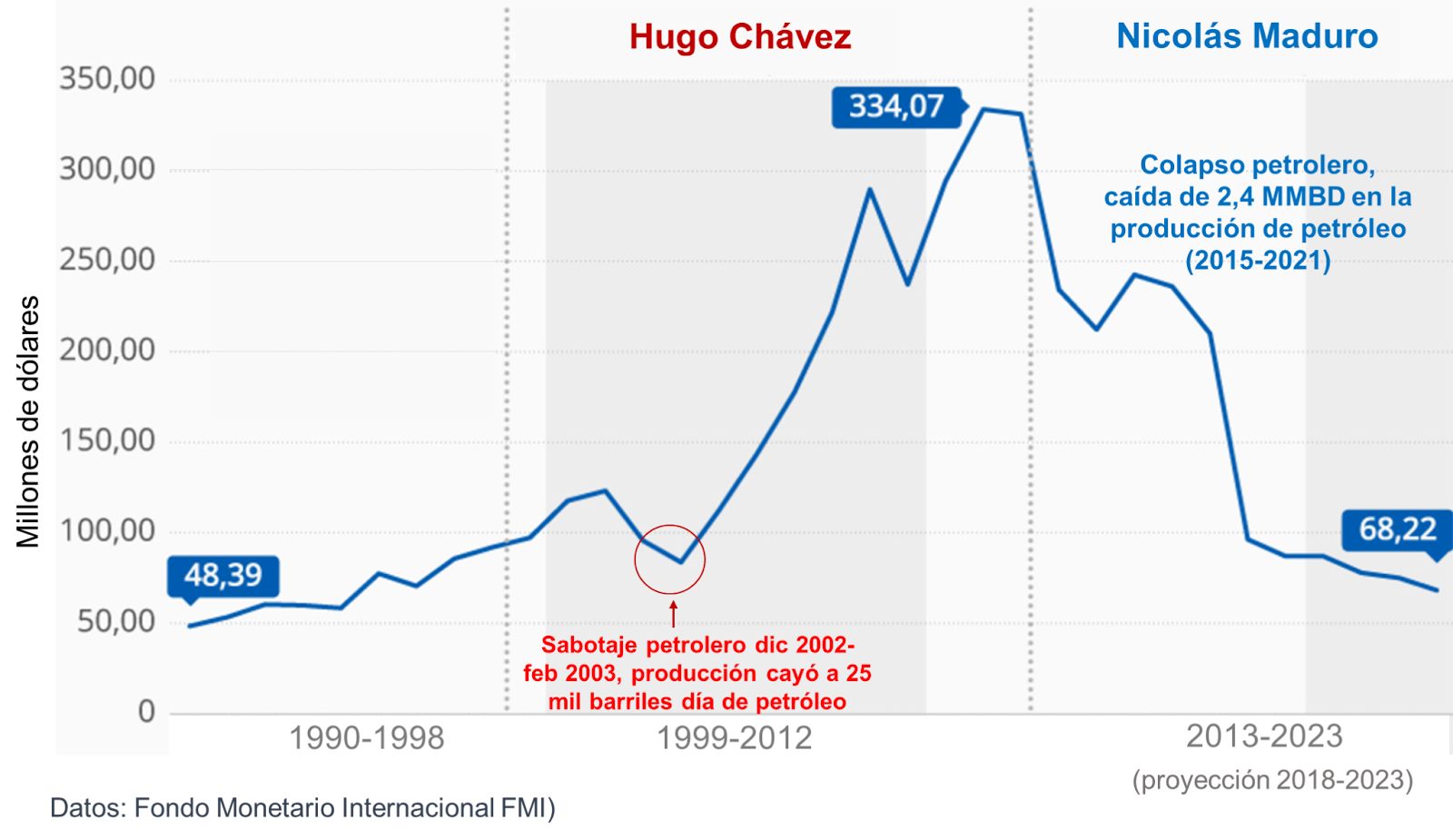

The recovery and stability of PDVSA’s production capacities, as well as an oil policy of defending the price and maximising oil tax revenue, fundamental pillars of the Petroleum Plena Policy for the period 2004-2014, were reflected positively in the country, with the income of 700 billion dollars from oil exports in the period and 350 billion dollars of contributions to the Treasury, which resulted in an undeniable period of economic growth and fair distribution of oil income in Venezuela.

GDP VENEZUELA (1990-2013)

Source: World Bank.

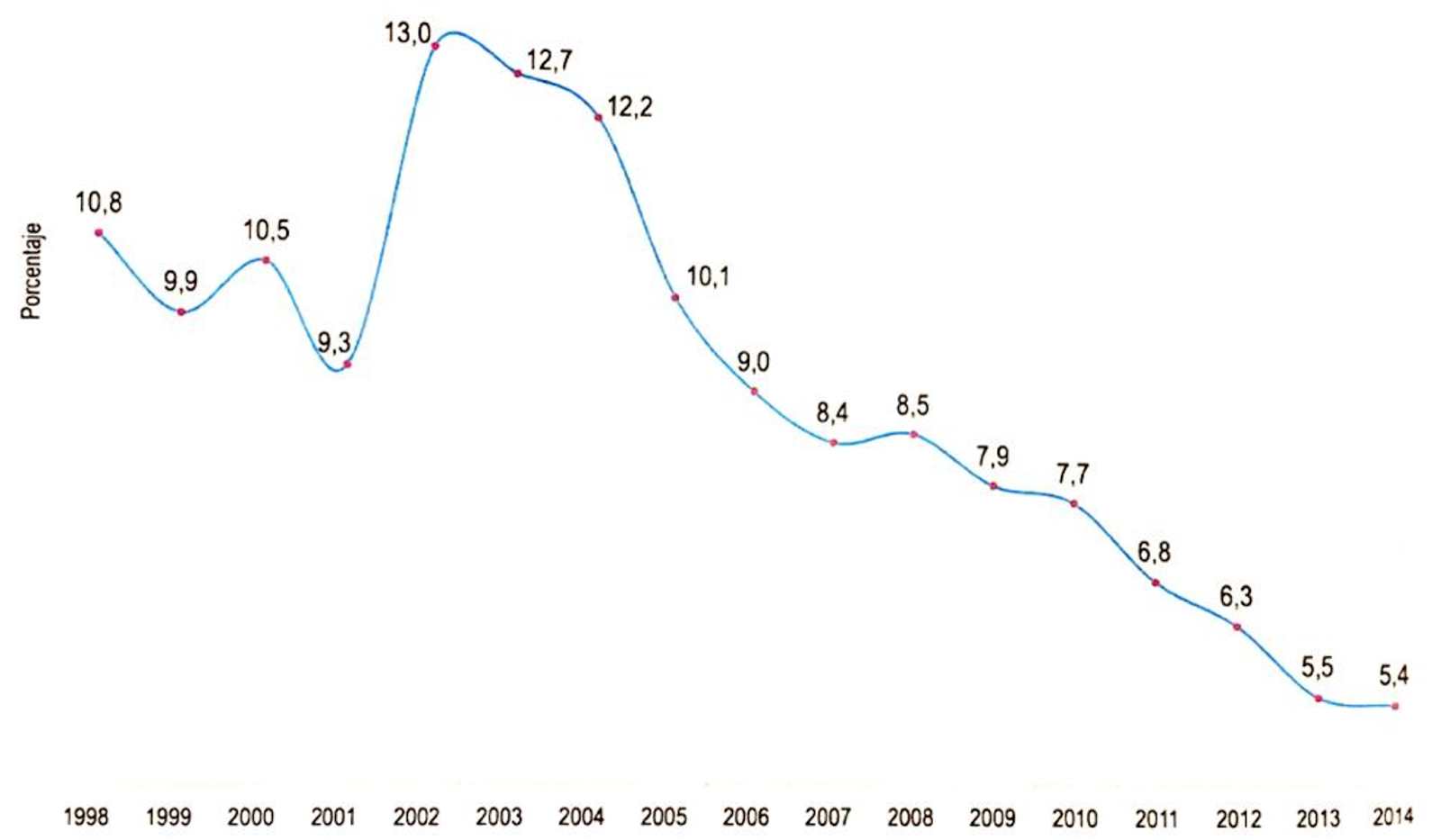

On the other hand, the restoration of the oil tax regime and the popular and revolutionary distribution of oil income, through the Social Development Funds and productive investments that allowed the Missions and large Social Missions to be sustained, as well as major national development projects, were reflected in overcoming the serious social problems of inequality and exclusion that keep the population at levels of poverty that were defeated during the period (2004-2014).

EXTREME POVERTY (1998-2014)

Source: UN/FAO 2014

HUMAN DEVELOPMENT INDEX (1980-2013)

Source: UNDP 2014

However, the current government has renounced this policy, and within the framework of the set of economic measures of “liberalisation of the economy” and shock policies implemented since 2018, it has chosen to hand over the management of the country’s most strategic sector to private agents and transnationals, thus giving sovereignty over the management of oil and making PDVSA, our national company, called to be in the Constitution and the LOH, the operator of our oil, a simple “agency” managing contracts.

THE FAILURE OF THE NEW “OIL OPENING”

At the end of 2017, as violence and political persecution raged within PDVSA and militarised the sector, the government decided to change the Petroleum Sovereignty Policy in force during President Chávez’s government to re-edit the fundamental aspects of the “Oil Opening” of the 1990s that caused the economic, political and social collapse of the country at the end of that decade.

This abandonment of the Petroleum Sovereignty Policy and the return to the “Oil Opening” has been developed as part of the government’s economic shock measures since 2018.

Irregular action with no legal basis

Since then, the government has used decrees, judgements and unconstitutional laws to repeal illegally –“de facto”– the hydrocarbon legal framework in force until 2017. Since the enactment of the so-called “Anti-blockade Law,” the government has reserved the power to “disapply” the Organic Law of Hydrocarbons (LOH)and other laws, as well as articles of the Constitution that limit or regulate its plans. A power that abolished the government in an absolutely unconstitutional manner and therefore null and void of any nullity.

The best oil fields in the country, which PDVSA between 2004-2014 successfully operated, have been illegally ceded to private operators through the figure of “Service Contracts”, a figure that seeks to evade the figure of Joint Venturescontemplated in the Organic Law of Hydrocarbons of the country.

On the other hand, in the Orinoco Petroleum Strip — where the world’s largest oil reserves are concentrated — the government has ceded the participation and control of PDVSA to the transnational minority partners in the country’s most critical Joint Ventures in contravention of both the Organic Hydrocarbons Law (LOH) and Decree 5,200 on the Nationalisation of the Orinoco Petroleum Strip (FPO) of 2007.

The government has illegally handed over control of oil operations, both in traditional areas of the west and east of the country and in the large Joint Ventures of the Orinoco Oil Strip, without any success.

Not only are these actions illegal — they violate the LOH and the Constitution — and are detrimental to the national interest, but they are based on the application of decrees, judgments and laws — such as the Anti-blocking Law — which, being unconstitutional and issued in contravention of all the mechanisms and requirements laid down in the Constitution in force for contracts of public interest, lack any legality, are null and void, and oil companies are unwilling — not worth it for them — to risk engaging in ‘secret’ and illegal businesses with a government which, moreover, has serious problems of legitimacy

None of the illegal figures that the government has created to manage the industry has yielded the results announced over and over again by the government regarding the increase in oil production.

X-ray of a failure (2014-2022)

Since 2015, the country’s average oil production has fallen steadily, and the capacities of PDVSA have been virtually dismantled, adding to the internal political persecution and the deterioration of the working, economic and social conditions of the workers who — together with the militarisation of the sector — have led to the departure of 30,000 specialised workers from PDVSA and the country.

The country’s oil production has been stagnating below 700 thousand barrels per day since 2019, and the country suffers a chronic shortage of fuels for its domestic market.

AVERAGE OIL PRODUCTION IN VENEZUELA (2013-2021)

Source: own production with PDVSA and OPEC data.

The collapse of all the operational areas

The country’s oil and gas production areas collapsed between 2015-2022, of around 2,3 million barrels of oil per day. This has been reflected in all the operational areas of the country, with greater emphasis on the oldest areas, with mature fields and deposits, centuries-old, where the lack of underground works has caused tremendous damage.

In the west of the country, both on Lake Maracaibo, on the East Coast and on the South of the Lake, production has collapsed dramatically, falling from 776 thousand barrels per day in 2013 to 128 thousand barrels per day in April this year. A fall of 84 %.

In the east of the country, including northern Monagas, production has fallen from 825 thousand barrels per day in 2013 to 179 thousand barrels per day in April 2022. A 78 % drop.

In the Orinoco Petroleum Strip, where the country’s largest reserves and the most important Joint Ventures are concentrated, production has fallen from 1.274 million barrels in 2013 to 365 thousand barrels per day in April. A 71 % drop.

Of the country’s total production, only 40 thousand barrels per day, i.e. 5 %, corresponds to the production of the so-called “Oil Services Contracts”.

OIL PRODUCTION BY AREA (2013-2021)

Source: own elaboration with PDVSA data.

The fall in oil production is compounded by the fall in gas production and the collapse of the national refining system, which has led to an acute shortage of fuels and inputs for the domestic market.

Capacity loss is not limited to PDVSA, its infrastructure and management and operational areas but extends to industry-related sectors.

The collapse of PDVSA’s productive capacities has dragged the entire sector of oil services, contractors and companies into the sector and is directly reflected in the fall in the economy of the whole country and the deterioration of its productive capacities.

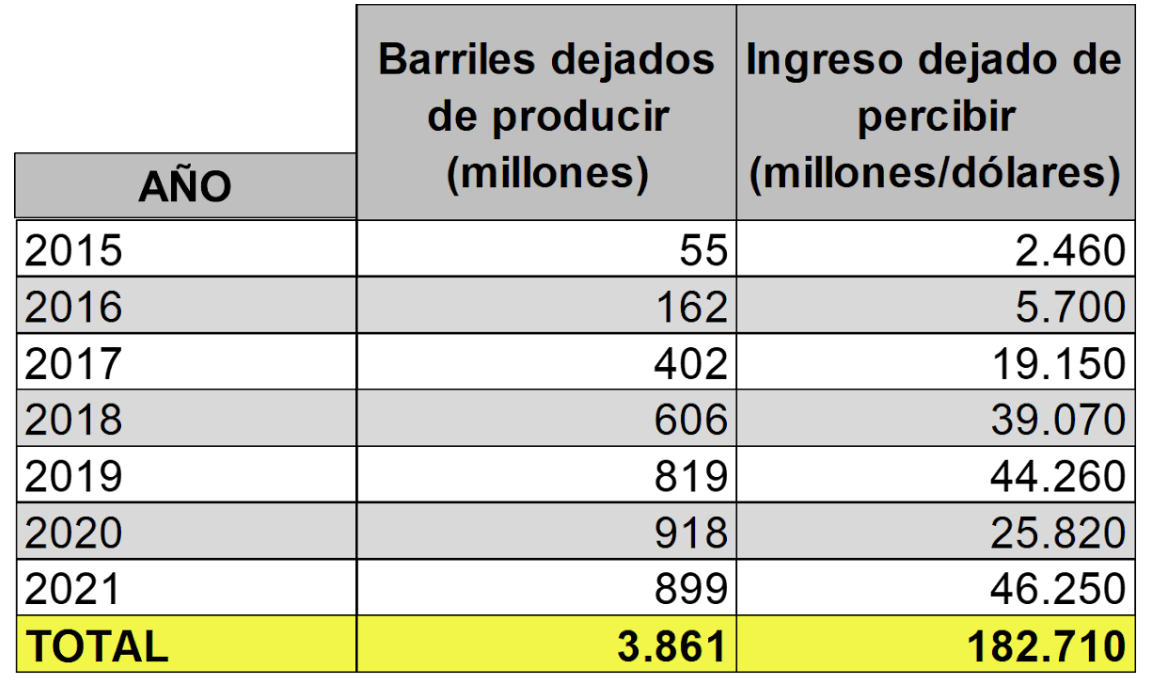

The collapse of oil income

The change in oil policy and the operational collapse of PDVSA, with the subsequent fall in the production and export of oil and products, has deprived the country of at least 182 billion dollars in this period (2015-2022), which has been reflected in a cumulative drop of more than 80 % of the country’s GDP, compared to 2013.

OIL INCOME COLLAPSE (2015-2021)

Source: own production with PDVSA and OPEC data.

The country has paid an immense cost (182 billion dollars) for the government’s political persecution against PDVSA and its workers, as well as for the abandonment of the Petroleum Sovereignty Policy, to implement a new and illegal “Oil Opening”.

ECONOMIC EFFECTS OF TWO OPPOSING OIL POLICIES GDP OF VENEZUELA (1999-2021)

Source: Statista, with its own edition.

Beyond government propaganda, the reality is overwhelming. The consequences for the country of the government’s New Petroleum Opening have been devastating and have affected the population’s quality of life. This collapse, and the severe crisis it has generated, confirm that Venezuela is a country with an eminent oil economy and needs oil revenues to sustain itself.

Between 2014-2022, as a result of the collapse of oil production and income, the country’s economy has accumulated an 83 % drop in GDP, and has been hit by hyperinflation and mega-devaluation of the national currency, the Bolivar — which is used only to pay salaries and bonds equivalent to $3.8 per month — all of which has led to widespread poverty of 90 % of the population and the exodus of more than 6 million Venezuelans, an unprecedented event in the country’s history.

A new “Oil Opening” that does not convince anyone

The government has been developing an aggressive propaganda campaign to create the mirage that the country’s situation has returned to “normality,” including the oil industry. For this campaign, they had the support of external factors and transnational companies with direct interests in the country, as well as agencies and “sites” representing bond and debt holders that make all kinds of speculation about the prospects of an “extraordinary recovery of the oil industry and the economy of the country”.

Furthermore, the government used the outgoing OPEC Secretary-General Mohammad Barkindo, who paid a lightning visit to the country on a PDVSA plane on May 6th, only to declare from Miraflores — where he was granted a decoration — that the country’s oil production has had a “ monumental recovery”. A strange and unusual statement in an OPEC Secretary-General, an organisation that usually does not engage in domestic policy issues of its member countries.

To advance its plans, the government — rather than statements and propaganda — needs oil companies that are willing to work within the framework of its New Petroleum Opening, for which it has indicated its willingness to hand over operational and commercial control, in addition to tax benefits, to the operators, in contravention of the current legal framework for the sector.

Until now, international oil companies have refused to operate within the framework of the secrecy and illegality that prevails in the sector, as well as amid an absolute lack of transparency in the management of public affairs, with a country ruined for nine years by an erratic economic direction that has decimated its productive capacities, with a total absence of the rule of law and institutionality.

In this dysfunctional environment and lacking legal framework, international oil companies such as Total and Equinor (who, in 2021, declared their investments in the country ‘lost’); just as Shell, Apex and even Russian Rosneft, have decided to abandontheir oil production operations in the country, while companies like ENI and Repsol, have decided to wait for any opportunity to recover the billions of dollars that PDVSA owes them.

The Chevron and the American License

In Venezuela’s government and political-economic sectors close to it, strong expectations have been created that the Chevron Corporation will re-start oil production operations in the country if there is an easing of sanctions by the Biden administration.

Chevron Corporation, present in the country since the beginning of the national oil industry, and one of the few North American companies that accepted the terms of migration to the Figure of Joint Ventures and the Nationalisation of the Petroleum Strip of the Orinoco, in the framework of the offensive of the Plena Petrolera Sovereignty, between 2004-2007, is a giant company with a worldwide production of 3 million barrels per day, but in Venezuela, it has participation mainly in two Joint Ventures: PetroBOSCAN and Petropiar, where Chevron has a minority share of 39.2 % and 30 % respectively.

The production of the Joint Ventures where Chevron participates was located in 2013 at 100 thousand barrels per day for PETROBOSCAN and 160 thousand barrels per day for Petropiar, for a total of 260 thousand barrels per day. However, by April of this year, the same Joint Ventures reported a production of 25 thousand barrels per day and 50 thousand barrels per day respectively for the total production in the country of 75 thousand barrels per day, of which Chevron corresponds 25 thousand barrels per day for its participation. A negligible volume for the U.S. giant that is obviously insufficient to replace Russian oil imports as the Maduro government has offered to the Biden administration.

However, despite the expectations created by the government and various sectors, the U.S. government only decided to renew — on the same terms today — the license to Chevron and other U.S. companies to maintain their facilities in the country, but without directly participating in oil production activities.

Maduro’s government is ready to violate the terms and conditions established in the Organic Law on Hydrocarbons, as well as the reserves enshrined in the Constitution for the activity and thus repeal the current legal framework for oil, as part of its policy of economic shock, liberalisation of the economy, privatisations and new Petroleum Opening, for which it intended to use the perfect excuse for the political sectors that still support it from Russia’s invasion of Ukraine.

However, the White House administration, through Juan Gonzalez, an advisor for Latin America, has been clear in stating that the lifting of sanctions and restrictions on the operations of U.S. companies in the country depends on the resumption and progress of political negotiations in Mexico, between the government and opposition factors, leading to guarantees for transparent elections in the country, something that does not seem to happen in the short term — at least in the terms expected to resolve the political crisis and institutional legitimacy in the country. At the moment, the government’s expectations have been frustrated by political reality.

REFINING

The national refining sector is strategic for the country, as its domestic crude processing capacities and fuel and input production must guarantee the supply of the country’s domestic market, sustaining domestic development while exporting processed products of higher added value.

Never before lacked fuels in the country

Never before in the country’s oil history had fuel shortages on the domestic market. Only during the Petroleum Sabotage (between 2002-2003), when the destabilising management paralysed and sabotage most of the country’s large refining complexes, damaging its infrastructure, the country experienced an acute shortage of fuels to the domestic market, which was immediately resolved that the refining and distribution operations of fuels, now by the New PDVSA, were restored.

As an essential part of the Petroleum Sovereignty Policy, the New PDVSA was identified as a fundamental priority of its management to guarantee the production and distribution of fuels for the national market, making investments and maintenance activities and plant stops in the country’s refineries to maintain them operating at their maximum capacity, managed and operated by qualified personnel and knowledgeable of the different technologies and particularities of each facility, built by the concessionaire companies in the country since the reform of the Hydrocarbons Law of 1943.

Investments and maintenance to refineries in the country (2002-2014)

Between 2002 and 2014, within the framework of the policy of the Petroleum Sovereignty and with the strategic objective of guaranteeing the production of oil and gas and the supply of fuels and inputs to the domestic market, PDVSA made significant investments in the various areas of oil business reaching the figure in this period of 120 billion dollars, of which 15,121 million dollars were allocated to the refining sector (15,121 million dollars), equivalent to 12.6 % of the total.

OIL INVESTMENTS OF PDVSA (2002-2014)

SOURCE: Audited Financial Statements of PDVSA, KPMG.